Nearly half of family-owned businesses lack a succession plan. That translates into another statistic: 12% of family-owned businesses fail after the third generation.

Imagine this: Jack Jillson runs a multi-billion-dollar company. Despite being 67 years old, he doesn’t intend to retire anytime soon. Even though Jack wants to travel from vacation home to vacation home with his wife during his golden years, he is uncertain how his children will react when it comes time for him to choose a successor. While he thinks it is his eldest son’s birthright to inherit the company, he firmly believes that his youngest daughter’s leadership style will be more conducive to the company’s success.

Due to his current predicament, Jack has decided to postpone his retirement indefinitely rather than make a decision that could upset others. However, that just means that the matter of succession will eventually fall to his board.

This is a common conundrum faced by family-run business owners. Other common succession-related problems they may encounter include:

- Worrying about their legacy and how it will live on through their successors

- Struggling to recognize and retain valuable management team members who aren’t in line for succession

- Communication difficulties with others regarding financial matters and personal goals during the succession planning process

- Having difficulty disconnecting from day-to-day responsibilities to focus on succession and long-term planning due to the fact that they are heavily involved in the company’s daily operations

- Feeling anxious that their successors aren’t ready to assume control even though they’re ready to step down

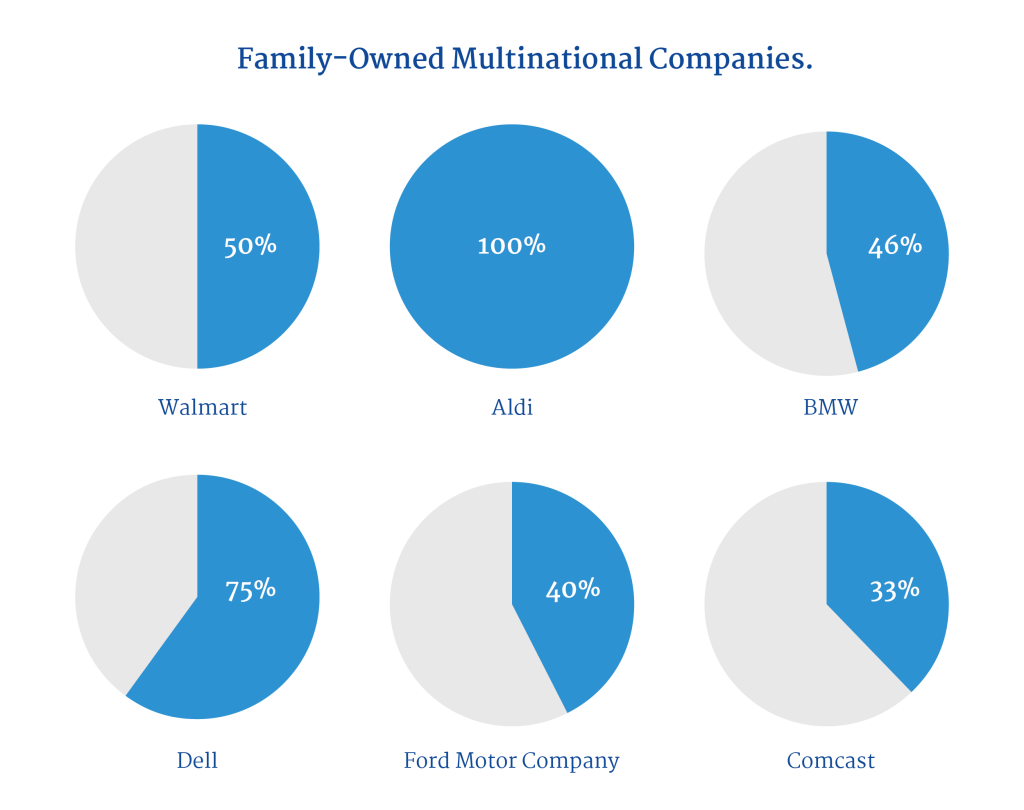

Jack Jillson and his company are fictitious, but several of the world’s most successful organizations are family-owned, including Walmart (50% family-owned), Aldi (100% family-owned), BMW (46% family-owned), Dell (75% family-owned), Ford Motor Company (40% family-owned), and Comcast (33% family-owned).

Many of these companies are not only family-owned but also family-run. For example, Rob Walton served as Walmart’s Chair of the Board. Elena Ford is Ford Motor Company’s Chief Customer Experience Officer and William Clay Ford Jr. serves as the company’s Executive Chair.

Succession Planning Tips for Family-Owned Businesses

You might be wondering how to balance business needs and family concerns in order to create a long-term governance plan that can help the business and family prosper together. The answer is a watertight succession plan.

A succession plan outlines who will replace your current corporate leaders. Its aim is to identify several possible successors. Succession plans also identify clear developmental goals for potential successors to ensure they can handle the responsibilities envisioned for them in their roles.

You can navigate the maze of succession planning for your family-owned business by following these six tips:

- Begin the process as soon as possible. It’s not enough to simply name a successor and hope for the best. Succession planning takes years, not moments, and requires careful decision-making and strategy. It is vital that you have time to train your successors and prepare them before handing over your corner office.

- Decide what you want to accomplish upfront. It is not uncommon for family-owned businesses to stay in the family, and it isn’t a sin to want your business to remain that way. It is important to be honest with yourself about it upfront if that is the case. Before you start planning, decide on the desired end result for your business and personal life. You will need to choose whether you want to keep the business (and manage succession planning) or sell it when you step down. If you choose to keep the business, you will also need to decide whether you want to hand the business over to a family member or appoint an external successor. In making this decision, you should consider the risk of interpersonal conflict. You will also need to work on an exit strategy or retirement plan.

- Conduct a thorough talent assessment. Your successor will need more than just technical skills to fill your boots. It is important to assess your talent pipeline as part of succession planning (including your children if you intend to keep the business in the family). A talent assessment should evaluate a person’s personality, skills, experience, and leadership style. It is also vital to consider whether they will fit into or add to the culture of the company.

- Don’t trap your children. Your children are not obligated to take over your company. Find out if it’s really the future that they envision for themselves before committing to backing them.

- Raise the bar for everyone. The most common complaint you’ll hear about family succession is that the bar is lower for family members. If you have your heart set on having a family member succeed you, it can be easy to turn a blind eye to their faults and weaknesses in favor of considering their talents and strengths. The best way to remedy this pitfall is by raising the bar for everyone; expect excellence from all your senior leaders, regardless of whether they’re blood relations or not (but especially if they’re blood relations).

- Get your mentor on. Following the identification of suitable successors and the announcement of your succession plan, the next step is to put all your efforts into practice. The first step is to take your potential successor (or successors) under your wing. The time has come to teach them the ropes and to start handing over some of your responsibilities to them. In addition, you should invest in any upskilling or additional education or training they may need.

Plan Your Succession to Ensure Your Legacy

Identifying the type of business that your successors will run is just as important as deciding who will run the business. Planning your succession requires considering not just who will succeed you, but also how the organization will function after they have taken over.

A proper and strategic transition of management and ownership offers many benefits for owners, like:

- The continuation and growth of the business and its assets

- The safeguarding of family relationships (a proper succession plan can prevent unnecessary tensions and conflicts)

- A chance for current leaders to retire knowing their business and legacy is in good hands (don’t be like Jack and give up on enjoying your golden years)

- The ability to control the process as opposed to letting your board decide in your absence

Creating a strategic and implementable succession plan is the best way to protect your business and your family.

Succession planning is sometimes complicated and conflict-prone. Fortunately, you’re not in it alone. One of our consultants would be happy to help you. You can click here to contact them.

About the Author

Milos Tucakovic is a Managing Partner at Stanton Chase Belgrade. He is also Stanton Chase’s Consumer Products and Services Global Practice Leader.

How Can We Help?

At Stanton Chase, we're more than just an executive search and leadership consulting firm. We're your partner in leadership.

Our approach is different. We believe in customized and personal executive search, executive assessment, board services, succession planning, and leadership onboarding support.

We believe in your potential to achieve greatness and we'll do everything we can to help you get there.

View All Services